A common question anybody struggling with payday debt has asked is, “Can I get another payday loan if I already have one?” The short answer is that yes, you can usually get another payday loan. However, you’ll likely have to turn to a different lender and the terms will be even worse than your original loan.

Featured Alternative: DebtHammer

- Break the borrowing cycle

- Can help with many types of debt, including payday and tribal loans

- Friendly and helpful customer support – no judgment

Disclaimer: Credit Summit may be affiliated with some of the companies mentioned in this article. Credit Summit may make money from advertisements or when you contact a company through our platform.

Table of Contents

Key Points

- The law doesn’t prevent lenders from giving out multiple payday loans

- Despite this, many lenders won’t give out a second loan until you’ve repaid the first one

- The more loans you get, the higher the interest rate you’ll pay, and the more likely you are to fall into the payday loan trap

- There are several alternatives to additional payday loans, including debt consolidation and Payday Alternative Loans

READ MORE: Payday loan consolidation

Instead of getting another loan, wouldn’t you rather get out of your current loans? Click here to learn how.

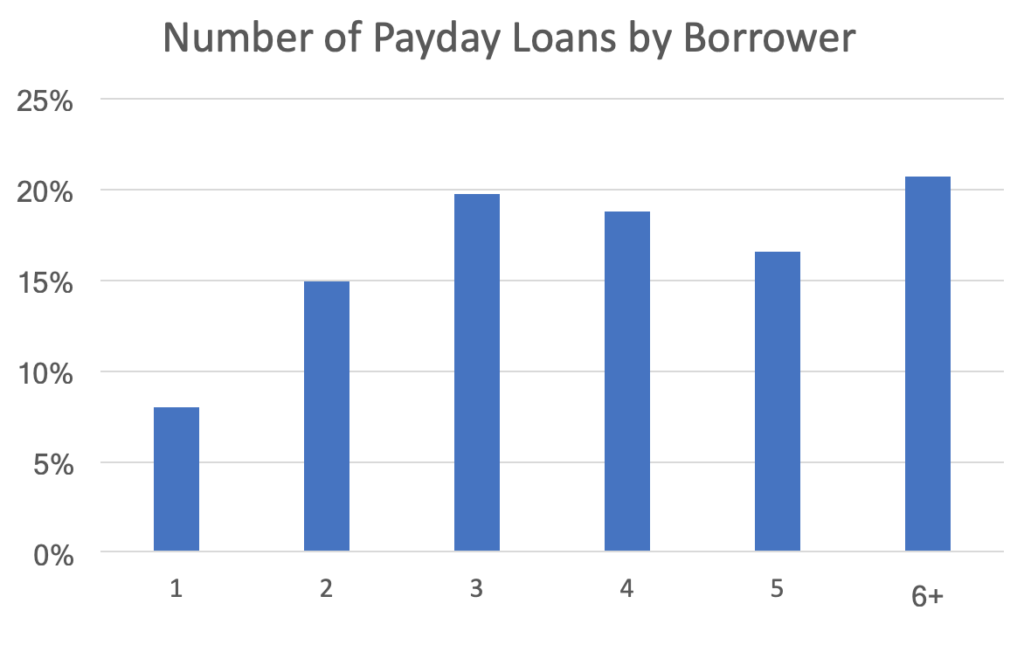

The Data: Most Borrowers Have More Than One Payday Loan

According to data from DebtHammer, the average payday borrower has 2.8 loans on average. Below, you can see the percentage of borrowers by the number of loans they have.

So the short answer is that yes, many people can get multiple payday loans.

Laws Don’t Prohibit Multiple Payday Loans

Payday loans — also called short-term loans, cash advances, and small personal loans — are regulated by state law. As of Jan. 1, 2023, payday lending is illegal in 18 states and the District of Columbia but legal in the other 32 states.

READ MORE: Can you get an extension on a payday loan?

How Many Payday Loans Can You Have at Once?

You can technically have several payday loans at once, but the situation isn’t that simple. This is because it depends on your location and the type of payday lender you are borrowing from. For example, in Washington state you can have up to eight payday loans at once, where as in Texas, there is a unified payday ordinance in 45 cities that allows no more than four installments and three rollovers. Your best option is to check your state’s payday lending laws or ask your lender.

Please remember:

- You should limit yourself to one or two payday loans at any time

- The payday loan trap is real and payday loans are expensive, which is why the industry is heavily regulated

- If you need to borrow another payday loan, try other alternatives first

- If you have no way to avoid another payday loan, do your research

Drowning in online payday loan debt?

Credit Summit may be able to help.

READ MORE: Best payday loan debt consolidation companies

The More Loans You Have, The Worse the Terms Will Be

Before you think about taking a second, third or fourth cash advance loan, you should consider the loan terms.

Pro tip: Because lenders have access to your credit report, they already know if you have outstanding loans. They know the types of loans, the loan terms, and other nitty-gritty of the loan agreement. They also know your credit score and credit history.

When they see you already have outstanding loans, they see you as riskier and more desperate. This means they will charge you higher interest rates than your first loan.

The more loans you have, the higher the interest rates and fees will get. The annual percentage rate of your second loan will almost definitely be higher than your first loan.

If you’re looking for a second payday loan because you think the first one is bad, don’t expect things to improve.

You should assume that every additional payday loan you get will have worse terms than the previous loan.

Instead, consider payday loan consolidation.

States With No Loan Limits

Some states have no loan limits. In Texas, for example, there is no legal limit to the amount a pay lender can give you. They could give you a loan for $100,000 if they wanted to (though obviously they wouldn’t).

So if you already have a $500 loan, the same lender or any other lender could give you another $500 loan.

States With Loan Limits — You Can Still Get a Second Loan

In Virginia, for example, the maximum loan amount is $500. But that does not mean you can only borrow $500. All this means is that any individual lender can only give you $500.

They can and will allow you to roll over your loan if you can’t pay at the due date. There may be additional fees associated with these. But they can’t increase your initial loan amount.

If you have a $500 loan from Speedy Cash, there’s nothing prohibiting Ace Express from giving you another $500 loan.

So even in states that have a loan limit, you can get a second payday loan. It just has to be from another lender.

The Consumer Financial Protection Bureau (CFPB) recently found that despite state protections and mandated repayment plans, payday loan borrowers are still paying significant late fees and rollover fees. This becomes even more of a problem for borrowers juggling multiple loans at once.

Online Lenders Often Break the Laws

If you visit a storefront payday lender, they are likely following the laws. Yes, they might be predatory scumbags, but they probably are licensed by the state.

However, once you go online, it’s the wild west. Some online lenders play by the rules, but many do not. Many of the online lenders are based offshore or on Indian reservations.

These lenders may not have a license and use loopholes like tribal immunity to bypass the laws. There is nothing — even the law — stopping them from giving you a second payday loan even if you already have one. And there’s no cap on the interest rate they charge. If you’re borrowing from a lender with tribal immunity, it’s likely you’re being charged APRs in the quadruple digits.

Pro tip: Do not submit any loan application to any online lender until you’ve thoroughly researched the lender. If you notice a pattern of complaints or see a notice that the lender is affiliated with a Native American tribe, choose a different lender. The Better Business Bureau pages for payday loan companies are riddled with complaints from customers whose loans violate their state laws. Tribal lenders are not obligated to follow state laws. It is your responsibility to ensure that you’re borrowing from a reputable lender.

READ MORE: About tribal loans and lenders to avoid

Will a Lender Give You Another Loan?

Even though the law allows you to get a second payday loan if you already have one, that doesn’t mean a lender will give you a second loan.

Payday loan lenders may be notorious for their quick and easy application process and minimal eligibility criteria,, but there is a process.

Before a lender gives you a loan, you give them permission to do a credit check on the loan application. When they do this, the credit bureaus — Experian, TransUnion and Equifax — report how many loans you have outstanding. Remember, the credit bureaus know everything about your transaction history. They know exactly how much debt you have. Then they decide on whether or. not they think you can repay it from your next paycheck.

- If a lender sees that you already have a loan, they may or may not be willing to give you a second one.

- If a lender sees that you already have two loans, they are even less likely to give you another one.

- If a lender sees you have five payday loans, they are significantly less likely to give you a sixth.

So the more payday loans you have, the less likely it is that you will get another one.

READ MORE: 15 reasons you were denied a payday loan

Should You Get a Payday Loan If You Already Have One?

You should not get another payday loan unless you’ve exhausted every other option, especially if you have already have one unpaid payday loan. Things can get ugly fast because of the high interest rates. You end up with a mountain of debt. It’s called the payday loan trap for a reason.

Before you know it, you have debt collectors blowing up every phone number you’ve ever had. You’re being charged nonpayment fees, NSF fees and overdraft fees. Your bank account is drained. Debt collection agencies are on your tail. All because you meant to borrow some money you intended to pay back on your next payday.

Why are payday loans so bad? Check out this video to learn more.

If you already have a payday loan, the best thing you can do is to exhaust every other alternative before you take out another.

Better Payday Loan Alternatives

Fortunately, there are several alternatives to taking out additional loans if you need to make ends meet.

- Credit unions: Credit unions and similar financial institutions often offer small loans at much lower rates. Most credit unions give multiple types of loans, such as personal loans, bad credit debt consolidation loans and/or Payday Alternative Loans (PALs). This varies between credit unions.

- Credit counseling: Credit counselors or nonprofit credit counseling agencies can offer financial advice to help you enroll in a debt management plan. Some will offer financial products that help with this. They may negotiate with your lender for better terms and offer personal finance advice on how to budget or how to improve your credit score.

- Renegotiate payment plans: Instead of taking out another loan, call your lender and ask for better payment terms, sometimes called an Extended Payment Plan (EPP). Even if they aren’t the friendliest, they do want their money back.

- Credit card balance transfer: Credit cards have a much lower APR than a typical short term loan. Many credit cards are meant for those with bad credit. Even better if you can get a balance transfer with 0% APR.

- Installment loans: If your credit is good enough to qualify (and there are even options for borrowers with bad credit), you can take out one new loan, ideally with a lower interest rate, and use that loan to repay your payday loans. Then pay off that loan with one lower monthly payment over a longer repayment term.

- Home equity loan or line of credit: If you’re a homeowner with significant equity in your home, you can usually borrow at an interest rate that’s far lower than most personal loans.

- Ask a family member for help: Nobody likes asking friends and family for money, but avoiding the payday loan trap is worth it. Ask your friends and family for a loan before taking out additional payday loans.

- Payday loan consolidation programs: A number of payday relief programs help negotiate the total debt burden for those struggling with payday debt.

READ MORE: 12 better payday loan alternatives

The Bottom Line

The simple answer is that yes, you technically can get another payday loan if you already have one. But the issue is far more complicated. You should not try to get more than one payday loan. You’ll end up stuck in the debt cycle, and it could take months or even years for your financial situation to recover. Instead, explore some of the other options listed here first.

FAQs

Cash advance apps, sometimes called paycheck advance apps, are similar to payday loans but don’t charge interest. Instead, there’s sometimes a small monthly subscription fee, and they ask you to “tip” them for the convenience of your loan. Using these wisely is a much better alternative to payday loans. Dave and Earnin are good options, or you can find more information and other recommendations here.

Though a payday lender can sue you if you don’t repay your payday loan, it’s important to know that you will not go to jail for lack of payment. The charges you would face would be civil charges, not criminal. You could still end up in jail, however, if you fail to appear in court or ignore a court order.

Debt collectors are notoriously aggressive, but you do have some protections through the Federal Trade Commission’s Fair Debt Collection Practices Act (FDCPA.) Federal law prevents the debt collection agency from calling you there if you inform a debt collector that you are not allowed to receive personal calls at work. If you believe your rights are being violated, notify the FTC or your state attorney general’s office.

A car title loan is a short-term loan (usually 30 days) where the loan is secured by the borrower’s vehicle. That means a borrower who is unable to repay a title loan is at risk of losing their car. Payday loans are unsecured and repaid from the borrower’s next paycheck. Both are high-interest loans and are typically considered predatory in nature.

Sources: