Table of Contents

Best Debt Relief Programs

Disclaimer: Credit Summit may be affiliated with some of the companies mentioned in this article. Credit Summit may make money from advertisements, or when you contact a company through our platform.

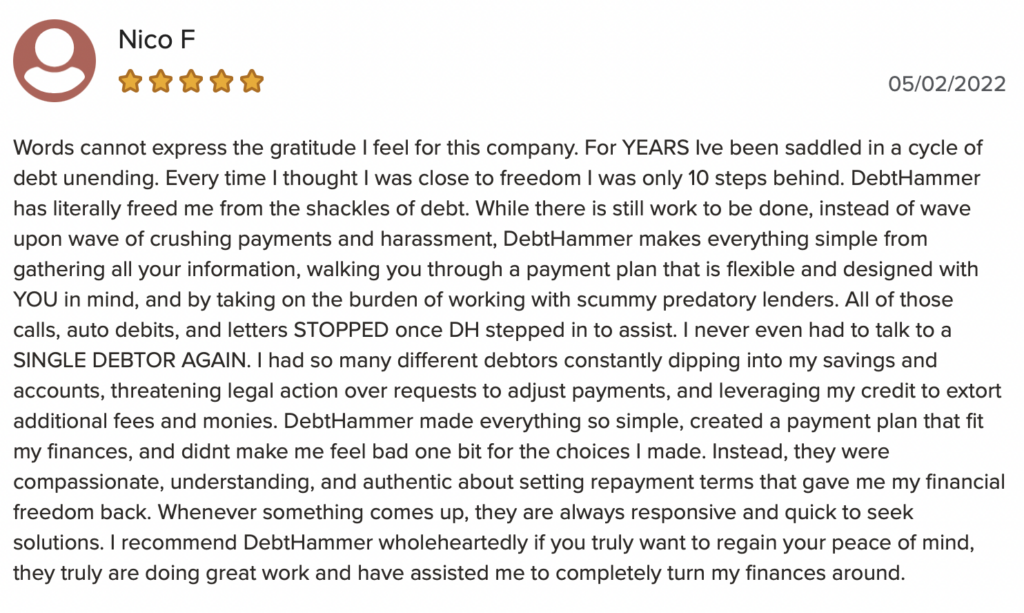

Best Overall: DebtHammer

Other Top Debt Relief Companies

Best for Simple Signup: National Debt Relief

Best for Income Tax Debt: Community Tax

Best for Unexpected Financial Hardship: Alleviate Financial

Legal Assistance

Best for Low-Income Households: Upsolve

The Upsolve app is free. However, you will still be required to pay for mandatory credit counseling and court fees. (The app can help you request a court-fee waiver if you’re eligible.)

The downside? Upsolve only works for Chapter 7 bankruptcy, and not everyone will be eligible to file for Chapter 7.

Upsolve has no reviews or complaints and is not rated by the BBB.

Best If You Think Your Rights Were Violated: Guardian Litigation Group

Guardian Litigation Group is a law firm that also offers debt settlement. This is a good choice if you believe that debt collectors have violated your rights under the Fair Debt Collection Practices Act. In addition to debt resolution services, the firm can advise you on bankruptcy, debt collection defense and tax debt relief.

Guardian Litigation doesn’t disclose fees and attempts to collect that information were rebuffed. However, a review on the firm’s BBB page – where the company gets 3.83 out of five stars and an A+ rating – indicates that it was charging one customer 27% of the enrolled debt.

Service is available in the following states: Colorado, Delaware, Georgia, Illinois, Kansas, Louisiana, Maine, Minnesota, Montana, Nevada, New Hampshire, New Jersey, North Dakota, Ohio, Pennsylvania, Rhode Island, South Carolina, Tennessee, Virginia, West Virginia, Wyoming

Guardian Litigation Group has earned 3.91 of 5 stars and an A+ rating from the BBB.

Credit Counseling

Best for Financial Counseling: GreenPath Financial Wellness

GreenPath is one of the biggest credit counseling agencies in the U.S. There are physical branches in several states, and services are also available online. GreenPath partners with hundreds of credit unions, banks and employers to offer services to members or workers.

GreenPath’s consultation and financial education services are free, but the company offers debt relief through Debt Management Plans. In a DMP, the credit counselor will contact your creditors and attempt to negotiate lower interest rates and better payment terms. DMPs are not a free service. There is a $50 fee to start a program and then a monthly fee that depends on the complexity of the plan, but is capped at $75.

GreenPath is a member of the National Foundation for Credit Counseling and it operates in all 50 states.

The company has 2.36 out of 5 stars and an A+ rating with the BBB.

Best for Transparency: American Consumer Credit Counseling

American Consumer Credit Counseling is a nonprofit credit counseling agency that offers Debt Management Plans and credit and bankruptcy counseling.

Like GreenPath’s service, ACCC will contact your creditors to try to get you lower interest rates and more favorable terms. If you commit to an ACCC Debt Management Plan, you will make a single monthly payment to ACCC, and the agency will then use that money to pay your creditors.

ACCC says it can take between two to ten years to complete a DMP. The company charges a $39 startup fee and a fee that ranges from $5 to $50 per month.

The agency has 4.95 of 5 stars and an A+ rating with the BBB.

What Do Debt Relief Companies Do?

Like the name sounds, a debt relief company offers programs that provide relief from crushing debts. They are also commonly referred to as It also may be referred to as debt resolution, debt negotiation or debt management programs. They accomplish this through three primary methods:

- Debt consolidation: This rolls your existing debt into one larger loan, ideally with a lower interest rate

- Debt settlement: This involves negotiating with creditors to reach a settlement agreement through which you pay less than you owe

- Debt Management Plan: A credit counseling agency will negotiate better terms and lower interest rates on your current debts, but you’ll still repay the full amount owed

The main goal of both types of programs is to make your monthly payments manageable and help get you out of debt faster.

How Debt Relief Companies Work

Most debt relief programs require you to complete a free consultation to determine whether you’re a good fit for either consolidation, settlement, credit counseling or bankruptcy. There is no commitment required.

For debt settlement, once you agree to a plan, the debt relief company will set up a savings account, and you’ll make regular deposits to that account instead of paying your monthly credit card bills. Once that savings account has accrued enough money, the company will use those funds to negotiate with creditors and establish a repayment term.

Most debt relief companies will charge a fee ranging from 15% to 27% of the total debt enrolled in the plan, and there may be an additional fee to maintain the savings account. However, you won’t be charged until your debts are resolved.

This means if you enroll a total amount of $20,000 in debt, you’ll pay between $3,000 to $5,600 to the debt settlement company, plus any additional fee for a savings account. In exchange, the American Fair Credit Council (AFCC) says you would save $6,000 on average (or 30% of your total enrolled debt) after the fees.

Types of Debt That Can Be Settled

Most unsecured debt is eligible to be settled. This includes credit card bills, personal loans, medical bills and some private student loans. However, not all unsecured debts are eligible. Types of unsecured debts that aren’t eligible include child support, alimony and tax debt. Tax debt has a different set of rules, which is why there are accounting companies that have made that their focus.

Secured debts, like mortgages and auto loans, are not eligible for settlement.

Debt Relief Options

There are a few different debt relief services available to you, depending on the amount of debt you have and the amount of time you can dedicate to getting out of debt.

1. Debt Settlement Program

A debt settlement company will ask you to stop making payments to your credit card companies and other creditors. Instead, you’ll put any money that was going to creditors into your designated savings account. When you’ve accumulated enough savings, the debt settlement service will negotiate on your behalf, contacting creditors and offering to settle your debts for less than you owe. Most of these settlements will be repaid over a set term, but some may be paid in one lump sum.

There are a couple of risks:

- Your credit score will initially decrease when you stop making payments because accounts can’t be settled until they’re considered delinquent (or charged off)

- Your creditors may refuse to negotiate, and then you’d have to pay any accrued interest and late fees

- After your debts have been settled, your accounts will be closed and marked as “settled.” While this in itself doesn’t hurt your credit score, potential employers or lenders will be able to see that you didn’t repay your debts in full.

However, if you can successfully complete the plan, a debt settlement can often be one of the cheapest ways to get out of debt, since you’re paying less than the full amount owed.

READ MORE: Best debt settlement companies

2. DIY debt relief

This is similar to a debt settlement program, except you set it up and negotiate on your own.

This is a good option if you don’t have enough debt to meet the minimum for a debt relief company, or if you want to try your hand at negotiating. You’ll save a significant amount in fees by doing it this way, but not every company is willing to settle, and debt settlement companies will usually already know which creditors are willing to work with you. Also, settling debts can be very time-consuming. You’ll need to be able to devote roughly the same amount of time you’d devote to a part-time job or side hustle.

3. Debt Consolidation

Many debt relief companies also offer debt consolidation services, or you can do this on your own. This involves getting a new loan or credit card, ideally with a lower interest rate, and using the new loan or card to pay off your other debts, consolidating them into one monthly payment. You’re credit score will need to be high enough to qualify for a new debt consolidation loan or credit card.

The two primary ways to consolidate debts are:

- Debt consolidation loans

- Balance transfer credit cards

If you’re doing this on your own, be sure to check interest rates, terms and fees before you commit to any new loan or credit card.

READ MORE: Debt settlement vs. debt consolidation

4. Debt Management Plans

Debt Management Plans are set up by a credit counselor or nonprofit credit counseling agency. These can be great option if you don’t meet the minimum debt requirement for debt settlement. The credit counselor will ask you to set aside money each month in a bank account. The credit counselor will contact your creditors and try to negotiate better loan terms and lower interest rates, then. set up a payment plan. However, you will repay the full amount you owe. The credit counselor will make the payments on your behalf from your savings account. They charge fees to administer Debt Management Plans, usually from $25 to $55 per month. Credit counselors also provide financial education and some other services for no charge. The National Foundation for Credit Counseling is a good place to look if you want recommendations.

The biggest drawbacks to Debt Management Plans are that only 50% to 70% of people who enroll actually complete the program, and you’ll repay the full amount you owe, plus the monthly fees.

READ MORE: Debt settlement vs. debt management

5. Bankruptcy

In 2022, 370,685 personal bankruptcy cases were filed in the U.S. While that number has been declining year-over-year, that’s still a significant number of households. The most common reasons for bankruptcy are income loss, medical expenses, or an unaffordable mortgage. There are two types of personal bankruptcy: Chapter 7 and Chapter 13. Most debt relief companies help with Chapter 7, but you’ll have to pass a state-specific means test to be eligible.

Pro tip: Contrary to popular belief, most people filing Chapter 7 don’t lose their homes and, in many cases, get to keep their vehicles.

Debt Relief’s Credit Score Impact

There is a common misconception that working with a debt relief company will do long-term damage to your credit score. Don’t let that deter you. The actual damage will depend on many factors, including the type of debt relief and your current score.

- Debt consolidation: If your credit score is currently good and you want to maintain that level, debt consolidation won’t negatively impact your score.

- Debt settlement: If you’ve already missed payments and your score is below the threshold for a consolidation loan (below about 600), debt settlement will knock it down temporarily, but it will rebound once your debts are repaid. It will NOT be damaged for seven years. However, as a condition of debt settlement, your settled accounts must be closed, and that will affect your credit utilization. The “settled” notation on those closed accounts will not hurt your credit score. However, it could indicate to potential landlords or employers that you didn’t fulfill the terms of a contract.

- DMPs: Debt Management Plans will require you to agree to close your credit accounts, which means your credit history will basically stop temporarily. This will push down your credit score. Once you’ve completed the DMP, the credit freeze is lifted, and you can open new accounts and your score will rebound. The notation signifying any DMP will not in itself hurt your credit score. It may even show lenders that you’ve put effort into fulfilling your financial obligations. When you agree to close all of your credit accounts, your credit history stops. Lenders and credit agencies like FICO and VantageScore use your credit history to generate a credit score. A temporary pause in your available credit may hurt your score.

- Bankruptcy: Chapter 7 bankruptcy won’t ruin your ability to get credit, but your score will take a big hit after filing and the bankruptcy will stay on your credit report for ten years.

Verify That the Company is Legitimate

Unfortunately, there are a lot of scammers out there who will make promises that are too good to be true. The Federal Trade Commission (FTC) offers a list of scam warning signs:

- If a company makes guarantees without speaking to your creditors first

- They try to charge upfront fees

- They don’t have a proven track record

- They are new and don’t appear to have more than a year of experience

- It’s difficult to find information about the company

- They don’t have Better Business Bureau (BBB) or Trustpilot pages or reviews (don’t worry about A+ ratings. Wade through the reviews and complaints and look for customer satisfaction and company responsiveness)

Carefully review the company’s website

You Shouldn’t Have to Pay any Fees Until Your Debts are Settled

The Federal Trade Commission (FTC) forbids debt settlement companies from charging fees before debts have been settled.

This means you shouldn’t be required to pay set-up or administrative fees for your program unless the program offers a money-back guarantee.

Risks of Professional Debt Relief

Though these companies will likely get you out of debt sooner than you could do it on your own, there are a few drawbacks:

- It won’t always work: Not all companies are willing to settle debts. However, legitimate companies should have a good idea of which companies are willing to settle, and they will know from your initial consultation whether or not they can help your financial situation.

- You may have to pay the IRS: Any settlement over $600 is considered taxable income, though there are exceptions for people who can prove hardship.

- Fees: You will pay a substantial fee for the services, but research shows the savings significantly outweigh the fees.

To learn more about debt relief, check out this video:

The Bottom Line

Dealing with debt is unpleasant, and almost everyone has faced a financial crisis at some point in their lives. If you’re losing sleep worrying about credit card debt, personal loans or medical debt, a debt relief company or debt management program may be able to ease your current financial situation.

Just be sure to choose a company that makes you feel comfortable about discussing personal issues. Also look for a proven track record, a professional-looking website and positive customer reviews.

FAQs

Accredited Debt Relief is a well-known debt relief company that helps customers with unsecured debts. The company was founded in 2008 and is based in San Diego, California.

Accredited Debt Relief offers a range of debt relief options. However, its services are not available in 19 states.

The International Association of Professional Debt Arbitrators (IAPDA) is a non-profit organization that provides accreditation and training for professionals in the debt relief industry. It was established in 2000.

Freedom Debt Relief is a well-known debt settlement company. However, it has been involved in several lawsuits involving complaints about its debt relief services over the years.

In 2019, the Federal Trade Commission filed a lawsuit against Freedom Debt Relief and its co-CEO Andrew Housser, alleging that the company made misleading claims to consumers. The lawsuit also alleged that the company charged upfront fees for its services, which is illegal under federal law. The case was settled in 2020 when Freedom Debt Relief agreed to pay $20 million in restitution.

The company has also faced lawsuits from several state attorneys general and multiple class action lawsuits over debt relief practices and fees.

It is important to note that a company that has faced lawsuits does not necessarily mean it is engaged in illegal or unethical practices. However, consumers should carefully research their options and consider the potential risks and benefits before enrolling in a debt relief program.