If you’re looking for a loan and trying to research Inbox Loan, you’d best look elsewhere. They’re no longer issuing loans. If you’re an existing Inbox Loan customer or are looking for information on inboxloan.net, read on.

Table of Contents

What Was Inbox Loan?

Inbox Loan was a short-term, small-balance, high-interest installment lender that operates online. They work with borrowers who have bad credit and position themselves as an alternative to payday loans, which they claim are too difficult to repay due to their single payoff requirement.

Their website stated: “Unlike traditional payday loans that expect you to pay everything back plus finance charges and interest in one lump sum payment, our fast cash installment loans let you pay back what you owe with fixed payments over time.”

Is Inbox Loan Licensed?

Inbox Loan’s address was in California, but they didn’t have a license from the state. They were what’s known as a tribal lender, which means that they follow the laws set forth by a Native American tribe over state regulations. They do obey applicable federal laws, but those don’t do much to reign in lending institutions.

Inbox Loan was an extension of the Kashia Band of Pomo Indians of the Stewarts Point Rancheria. As a tribal lender, they benefit from tribal immunity, which means that they’re essentially immune to lawsuits. Tribal lenders use that privilege primarily to charge interest rates that are far higher than the legal limits.

Typical Loan Terms

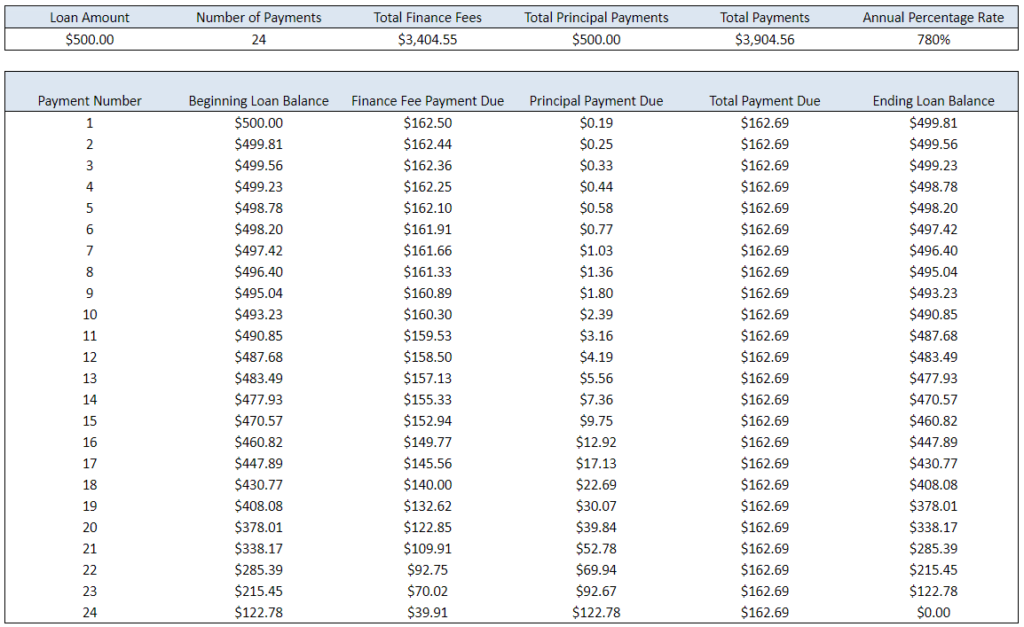

Inbox Loan’s sample loan drives home just how expensive their installment loans could be for those who couldn’t pay them off early. A $500 loan from them would end up costing a borrower a whopping $3,404.55 in interest over a 48-week repayment term. That’s almost seven times the initial loan amount in interest!

Online Reputation

Better Business Bureau

The Better Business Bureau (BBB) reports that the lender is out of business.

Lawsuits

It’s always a good idea to look for any lawsuits against a lender before working with them, too. It’s a red flag that consumers should never ignore. There’s been at least one lawsuit against Inbox Loan despite its tribal status.

Shannon Gonzalez and Bronal Gary brought a class-action suit against the company on behalf of the people of North Carolina for their usurious interest rates. The court dismissed the case because of Inbox Loan’s tribal immunity.

How to Apply to Inbox Loan

Inbox Loan’s primary website states that they’re no longer originating loans, and Inbox Credit appears not to work. Since it’s a completely online lender with no storefront, it seems that applying for one of their loans is impossible for now.

However, there is a lender called Index Loans (inboxloan.net) that sounds similar and may be related, but a lengthy disclaimer states that Inbox Loans will not actually issue loans but instead matches borrowers and lenders. Regardless of whether there’s a connection, it’s best to avoid inboxloan.net, since there’s no way of knowing specifics of any offer without submitting your personal information.

Better Alternatives to Inbox Loan

People usually turn to lenders like Inbox Loan because they don’t think they have any alternative or don’t know the risks involved. At this point in the Inbox Loan review, everyone should be well aware of the problems they pose. What might not be as clear is what other options are available to people who need cash but struggle with credit.

Here are some options that are much more affordable:

- Paycheck Advance Apps: These apps, sometimes also called cash advance apps, aren’t technically loans, but that means that there’s no interest! They allow users to access their earnings in a pay period before the check comes through. For example, someone who won’t get their $2,000 paycheck until the 15th could access $200 of the amount she’d already earned by the 8th using one of these apps.

- Peer-to-Peer Loans: Another great way to get funding in today’s market is by working with an individual lender from an app like Peerform, Prosper, or Lending Club. They connect private borrowers and lenders and let them negotiate terms. While the rates will still be expensive for people with bad credit, they shouldn’t be anywhere near 700%.

- Secured Loans: Lenders don’t want to take a chance on someone who might not pay them back, but secured loans allow borrowers with bad credit to get around that problem. Lenders can always seize the collateral to recoup their losses.

Any of these would be better options than Inbox Loan for someone struggling with bad credit who needs cash. The paycheck advance apps are probably the best place to start, but they’re the least sustainable over the long term. For those who need to fund larger bills, secured or peer-to-peer loans would be better.

The Bottom Line

If you were looking for an Inbox Loan review that would simply tell you whether or not to bother with the business, here’s your answer: Don’t waste your time. The original lender is no longer issuing loans. A website with a similar URL may or may not be related, but due to the lack of clarity we do not recommend it.

If you need to take on debt to cover yourself in an emergency, try one of the options that we mentioned above. Once the crisis has passed, do your best to adjust your finances so that you don’t need to take on debt again. Borrowing money from others is rarely a sustainable plan. Reduce your expenses or increase your earning power so you don’t need to do it anymore. If you need help getting your finances in order, talk to a credit counselor. Their services are free, and there’s almost certainly a helpful one near you. Find one today!