Update: Silver Cloud Financial is No Longer Issuing New Loans

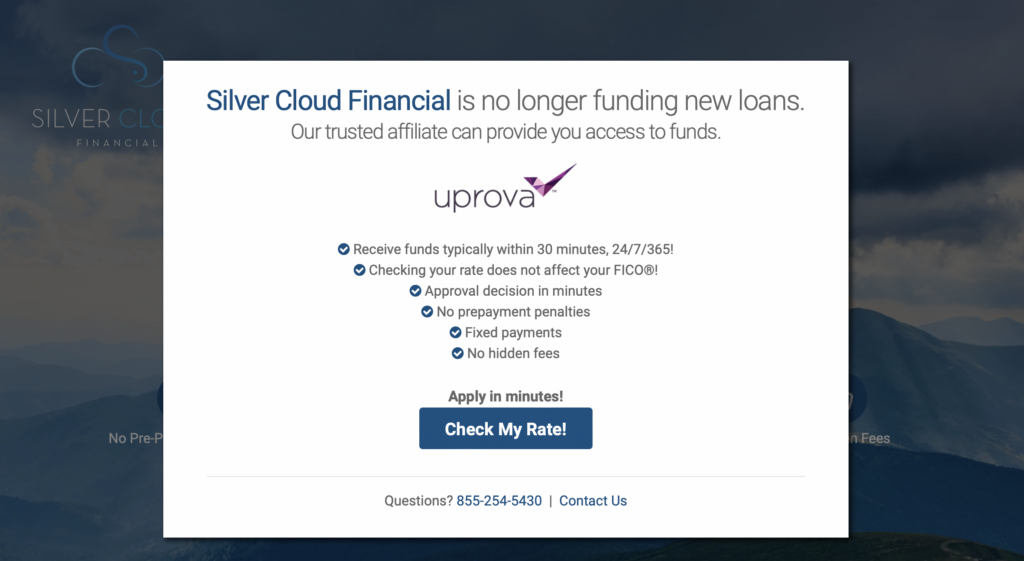

When you open Silver Cloud’s website, a popup appears stating that Silver Cloud is no longer issuing new loans. Unless you’ve already borrowed money through Silver Cloud and are experiencing problems, you’ll need to choose another lender. Silver Cloud suggests “trusted partner” Uprova.

Warning! Don't take a tribal loan just yet. See what better options you may be eligible for.

I acknowledge that I have read and agree to the Terms of Service, and agree to be contacted about my situation by email, sms, and / or phone including automated dialers by Credit Summit and its affiliates.

Tell us about your loans

Please enter the lender and the approximate amount you owe. Don't worry if it's not exact.

Connecting You With a Debt Expert

Please stay with us for a moment so we can review your options.

Live chat...

What is Silver Cloud Financial?

Silver Cloud Financial was an online lender that provides short-term installment loans. They were what’s known as a tribal lender, which is a lender located on Native American tribal land. They do this because Native American tribes have sovereign immunity, which allows them to sidestep state laws capping interest rates.

That means Silver Cloud Financial’s interest rates were significantly higher than the vast majority of lenders.

There was a significant lawsuit against Silver Cloud Financial as recently as 2017. The Consumer Financial Protection Bureau (CFPB) sued them — and three other online lenders — for collecting debts from consumers who didn’t actually owe them. They eventually dropped the suit, perhaps because they struggled to pierce the veil of sovereign immunity.

A couple of years later, borrowers also brought a class-action suit against the same four lenders for charging interest rates that exceeded state limits. Wisely, they’re taking the strategy of disputing that the lenders actually belong to the Native American tribes that they’re using to claim sovereign immunity. Time will tell if they’re able to break the connection.

Lenders like Silver Cloud Financial tend to attract people who don’t think they have any other option. They usually can’t get any help from friends or family or access traditional banking options due to their low credit scores.

People in that situation definitely have access to fewer credit options than people with better credit scores, but that doesn’t mean that they have to rely on tribal lenders. There are plenty of options out there that will be much more affordable. These are some of our favorites:

Paycheck Advance Apps: Paycheck advance apps are perhaps the best initial alternative to payday and tribal loans. They allow borrowers to tap into their earnings during a pay period before their paycheck goes out. For those who are short a few hundred dollars and are just waiting until their paycheck arrives, these are perfect. They carry no interest and only require users to pay a small monthly fee to receive their services.

Payday Alternative Loans: Payday loans are so prohibitively expensive that the government had to step in and help. Federal credit unions now offer payday alternative loans that provide all of the same benefits (short-term, small balance loans) to consumers in need of emergency funding. The key difference is that they come without the price tag.

Both of these options would be superior to an installment loan from Silver Cloud Financial or Uprova. They’re far less expensive, but still available to borrowers who are struggling with their creditworthiness.

The Bottom Line

If you wanted a Silver Cloud Financial review that would summarize whether or not you should work with the lender more succinctly, then here you go: Take your business elsewhere. Silver Cloud isn’t even funding new loans.

They’re too expensive to do much more than delay a financial emergency, and their disregard for state laws makes them particularly dangerous. If you can use one of the lending options we mentioned above, you’ll be much better off financially.

Even better, try to avoid taking on debt in the first place. If you find yourself needing to resort to external funding consistently, you’ll need to reduce your expenses or increase your income to become financially stable.

If you need help, talk to a credit counselor. They’re experts in personal finance and their services are free. Find one near you today!