If you’re stuck in payday debt and interested in payday loan consolidation programs, you’re on the right track.

Payday loan consolidation programs or loans allow you to combine all your loans into a single, lower interest loan.

However, you also need to watch out for payday loan consolidation scams.

The payday industry is full of fraudsters and scammers — tribal lenders that break the law, and companies that pretend to be helping, only to take your hard-earned money away.

Looking to Consolidate Your Loans?

Don’t fall into another scam. We’ll help you pick a legit consolidation company that best suits your needs.

Disclaimer: Credit Summit may be affiliated with some of the companies mentioned in this article. Credit Summit may make money from advertisements, or when you contact a company through our platform.

Table of Contents

Are Payday Loan Consolidation Companies Real or a Ripoff?

There are certainly a few legitimate payday loan consolidation companies out there that genuinely help borrowers reduce their overall debt. On the other end of the spectrum, there are also payday relief companies that are scammers. And in the middle, you have debt consolidation companies that are legit, but don’t help as advertised for every situation.

Picking a consolidation company isn’t easy, but that’s what we’re here for. We recommend DebtHammer, which works with debts of all sizes and only takes on clients they can help.

If you’d like to talk to a human who can help you choose the best program for you, feel free to request a free consultation here and we’ll do our best to help.

7 Ways to Recognize a Payday Loan Consolidation Scam

1. Bad Better Business Bureau Ratings

The first place to go to see if a consolidation company is legit is the Better Business Bureau.

You should realize that not every company is going to have pristine reviews, especially in this industry. But a legitimate consolidation company or lender will at least respond and attempt to resolve negative reviews and complaints. If a business doesn’t bother to respond to disputes, or there are too many reports of scams, than run. This is likely a consolidation scam.

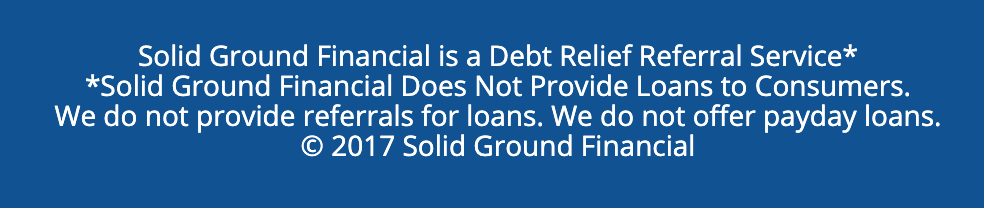

2. Are They Just a Middleman?

The payday industry is full of middlemen called “lead generators.” These companies don’t actually give out loans or consolidation, they just use internet marketing to capture contact information, then sell it to the highest bidder.

Usually these lead generation sites will advertise as if they are a company, but really are a referral service. For example, check out this disclaimer on Solid Ground Financial.

This doesn’t necessarily mean that they are a scam. But you need to vet the loan provider that you are actually dealing with. Do not trust these middlemen to vet them.

3. Tribal Affiliations

If you see the mention of any Indian/Native American tribe, you can rest assured that this is not a legitimate consolidation company.

Sometimes they will claim they have a “license,” but that license hasn’t been granted to them by the government. It’s granted by the Indian Tribe.

Be sure to Google the address as well. If it’s located on tribal land, find another lender.

Payday loan scammers often use “tribal immunity” to break the laws. If you see anything related to an Indian reservation, run!

READ MORE: Tribal loans and tribal lenders to avoid

4. No Real Business Records

If you can’t find any records of the business, it’s probably a scam, or, at best, a middleman. Any real business will have a physical address and an official business name, which you can use to look them up in whichever states they claim to operate.

Even scammers can get an LLC — it only takes 10 minutes to set up on Legal Zoom. So if any so-called consolidation company doesn’t have a business record, it’s a scam.

5. No Lending License

Not all payday loan consolidation companies offer loans, but the ones that offer debt consolidation loans are required by law to have a lending license. Usually there will be a license record on their website, but that can be faked. So go to your state’s licensing website and be sure you can look up the business name. Here’s an example for the state of Texas: https://occc.texas.gov/industry/regulated-lenders

No license? Probably a scam.

6. No Address

If you can’t find a physical address for the company, find another lender. It’s that simple. Any legit firm will have an address on their website. And of course, be sure to look this up on Google maps as well. No address? Probably a scam.

7. They Demand an Upfront Fee

Legitimate debt settlement companies will usually offer a free initial consultation to learn more about your financial situation. If a company demands money in advance, or something that sounds odd, like payments by gift card, do not hand over any money.

Pro tip: Consolidation isn’t just for payday loan debt. You can also roll in your credit card debt and medical bills.

READ MORE: Step-by-step guide to payday loan consolidation

Protect Yourself

If an offer seems fishy, don’t be afraid to ask questions. Don’t provide your social security number, bank account information, debit card details, a phone number or any other personal information unless you’re 100% certain a company is legit.

READ ALSO: How to spot payday loan collection scams

If You’ve Already Been Scammed

If you suspect you’ve fallen victim to a loan scam, contact local law enforcement as quickly as possible. Also notify your state’s attorney general and, if the company operates in another state or outside the U.S., alert the FBI. The Federal Trade Commission (FTC) and Consumer Financial Protection Bureau (CFPB) also will be helpful allies.

READ MORE: Legitimate payday loan consolidation companies that will help you get relief

The Bottom Line

Consolidating your payday loans is a good idea, but beware of debt consolidation scams. They’re around every corner. But by following these guidelines you’ll be able to spot the red flags and protect yourself.

READ MORE: Step-by-step guide to payday loan consolidation

FAQs

Many different forms of loans can be consolidated, including certain kinds of student loans. If you have federal student loans, they’re eligible for consolidation, while some private student loans may not be. You could end up paying more in the long run, though.

If the debt collectors are hounding you, the Fair Debt Collection Practices Act is a federal law that lays out the rules about what third-party debt collectors can and cannot do. The law “prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.”

Payday loans are small short-term loans with tight repayment deadlines. Payday loan companies profit from borrowers’ inability to repay the loan in two weeks, forcing you to roll over. your initial loan into a new loan. Personal loans are installment loans for larger amounts of money that are repaid over a longer period of time. If your credit score is high enough, a personal loan will be a much better option because of lower interest rates and more flexible monthly payments. Learn more about some top personal loan options.