National Debt Relief promises effective relief for serious debt problems. Let’s see if they deliver on that promise.

A Featured Alternative: DebtHammer

- Can help with many types of debt, including payday and credit card

- Extremely transparent process, no shadiness

- Friendly and helpful customer support – no judgment

Table of Contents

National Debt Relief at a Glance

National Debt Relief is a debt settlement company. Debt settlement can be an effective way to get out of debt, especially if you have more debt than you can

| Do they offer a free consultation? | Yes |

| How to get started | Go to the National Debt Relief website and click “Apply Now.” |

| Fees | 15% to 25% of your enrolled debt |

| How it works | You’ll have a free initial consultation to analyze your situation and recommend a solution. From there, the process will depend on the solution you choose. |

| Who owns National Debt Solutions | Alex Kleyner, CEO and Co-Founder |

| Company address and phone number | 180 Maiden Lane, 30th Floor, New York, NY 10038; (800) 300-9550; nationaldebtrelief.com |

| BBB rating | 4.59 of 5 stars from 1,619 reviews |

| Trustpilot rating | 4.7 of 5 stars from 35,974 reviews |

| Minimum debt settled | $10,000 |

| Noteworthy features | Customer reviews are among the best in the debt settlement industry. Accredited by the International Association of Professional Debt Arbitrators (IAPDA) and the American Association for Debt Resolution (formerly known as the American Fair Credit Council or AFCC) |

National Debt Relief: What You Need to Know

Like all debt settlement companies, National Debt Relief works with unsecured debts, like credit card debt, medical debt, personal loans, payday loans, and private student loans. They will not help you with federal student loans, mortgages, car loans, or other secured debts.

Debt settlement involves negotiating with your creditors. Negotiators certified through the International Association of Professional Debt Arbitrators will contact your creditors and offer them less than what you actually owe. If the creditor accepts, your account will be permanently closed.

You won’t pay anything until your debts are settled. National Debt Relief’s fee will be a percentage of your enrolled debts.

The National Debt Relief website shows multiple examples of clients who reduced their total debt load by as much as 50%. The fine print at the bottom of that page says this:

“Clients who are able to stay with the program and get all their debt settled realize approximate savings of 46% before fees, or 25% including our fees, over 24 to 48 months. All claims are based on enrolled debts.”

While National Debt Relief is a reputable debt settlement company, the entire debt settlement process has inherent risks and disadvantages, which all debt settlement companies share.

READ MORE: Debt settlement fees

What Makes National Debt Relief Stand Out

National Debt Relief is a debt settlement company. They do not provide credit counseling, debt consolidation loans, or other debt relief services. They may be able to refer you to a tax adviser or bankruptcy attorney in some states.

Debt Consolidation

The National Debt Relief program is a form of debt consolidation: you will replace all of your debt payments with a single payment to your settlement account. The difference between National Debt Relief’s plan and a debt consolidation loan is that you will stop making payments without the consent of your creditors.

READ MORE: Debt consolidation vs. debt settlement

Debt Reduction

If you stick with the debt settlement process – it can take two to four years – your debts can be reduced by an average of 25%, including fees.

Eligible Types of Debt

Note that National Debt Relief only helps settle unsecured debts.

Eligible debts include:

- Credit card bills

- Medical bills

- Personal loans

- Payday loans

- Private student loans

Secured loans, like mortgages and auto loans, are not eligible for debt settlement.

Customer Reviews

National Debt Relief provides essentially the same services as other debt settlement companies. The main factor setting it apart is its reputation for first-class customer service and strong customer reviews.

However, that doesn’t mean all customers are satisfied with the service. National Debt Relief also has a number of dissatisfied clients who say their experiences weren’t positive.

How to Sign Up

You can sign up by calling National Debt Relief’s toll-free number at 800-300-9550 or by clicking “Apply Now” on the company’s website.

Your first step will be a free counseling session. Your counselor will need a complete list of your debts, income, and living expenses to help you effectively.

Pro tip: Remember that the counselor has a financial incentive to recommend a debt settlement program that will make money for the company. Don’t let yourself be pressured.

READ MORE: Is debt settlement the best way to get out of debt?

How Does National Debt Relief Work?

Here’s what will happen if you choose National Debt Relief.

- Free consultation. A counselor will review your situation in detail and explain your options. The counselor may recommend National Debt Relief’s debt settlement service.

- Stop paying debts. Instead of paying your lenders and creditors, you’ll make payments into a dedicated savings account, which is under your control. This stage may take a significant amount of time, from months to a year or more. You could rack up some late fees during this time, and debt collectors will start calling.

- Negotiation. When you have enough in your account to offer a settlement, National Debt Relief will negotiate with your creditors, proposing that they close the account for a payment that’s less than you actually owe.

- Settlement. Once a settlement is negotiated, you will authorize repayment from your debt settlement account.

- Payment. When all of your enrolled debts are settled, you will pay a percentage of the enrolled debt to National Debt Relief.

Once a debt is settled, it’s gone. You have no further obligation to the creditor.

Disadvantages of Using National Debt Relief

Debt settlement also has serious disadvantages.

- Collection efforts. When you stop making your minimum payments, you can expect collection efforts to intensify. Collectors will pursue you.

- Credit score damage. Your payment stop will result in late payments. Accounts may be charged off and sent to collections. Your credit score will reflect that.

- Potential lawsuits. A creditor could sue you when you stop your payments. You will have to respond and appear in court, and your wages could be garnished. Participation in a debt settlement program is not a viable defense in a creditor lawsuit.

- Extended timeframe. It will usually take you two to four years to complete a debt settlement program.

- Tax liabilities. If more than $600 in debt is forgiven through your settlements, the amount forgiven must be reported to the IRS. It will be taxed as income.

Debt settlement companies won’t always explain the disadvantages fully.

Pro tip: It’s worth noting that there have been several complaints about National Debt Relief, so make sure to do your research.

READ MORE: Complete guide to debt relief programs

Is National Debt Relief Legitimate?

Yes. National Debt Relief has been in business since 2009 and has served over 400,000 clients. Customer reviews are generally positive. There is no indication that the company is a scam.

We found no record of any lawsuits or regulatory actions involving National Debt Relief.

Pros and Cons

Choosing to work with National Debt Relief has some benefits, but also some drawbacks.

Pros

- Well recognized in the industry

- Positive customer reviews

- Free consultation

- Referrals to other debt relief providers

- No upfront fees

- Reasonable costs: National Debt Relief’s fee is near the average for its industry

Cons

- Cannot work with all debts

- May be more expensive than other debt relief options

- Some creditors may not be willing to negotiate

- It can take years to get results

- You may face aggressive collection actions or creditor lawsuits

- Significant credit score damage

- Charge-offs will appear on your credit reports until your settlements have been paid

- You may owe back taxes on forgiven debts

- Not available in Georgia, Connecticut, Kansas, New Hampshire, Maine, Oregon, Vermont, South Carolina, or West Virginia

READ MORE: Pros and cons of debt settlement

Who Should Use National Debt Relief

Like all forms of debt relief, debt settlement isn’t for everyone. These are indications that you are a good candidate for debt settlement.

- Your debt is overwhelming

- You’re struggling to keep up with your monthly payment

- You’re trying to avoid filing for bankruptcy, or you are not eligible for Chapter 7 bankruptcy

- You’re trying to avoid handling debt settlement on your own

- You’re no longer concerned about your credit score: you just want to get out of debt

If that sounds like you, debt settlement could be one of your better options.

Who Should Not Use National Debt Relief

There are also people who probably should not rely on debt settlement.

- You don’t want to pay for debt settlement

- You have less than $7,500 in unsecured debt

- You still have relatively good credit

- Your debt is primarily business debt

- You are planning to take a major loan – for example, apply for a mortgage or auto loan – soon

- You are eligible for Chapter 7 bankruptcy and have relatively few assets

Pro tip: If you have less than $6,000 in debt, you won’t be eligible for most debt settlement programs. In that instance, your next best step would be to consult a nonprofit credit counseling agency. They can negotiate lower interest rates with your credit card companies and set up a Debt Management Plan (DMP) for you. However, you will pay a monthly fee to the agency to administer the plan. Be sure to ask about the fees in your initial consultation, and seek out agencies with the lowest monthly fees.

READ MORE: Best debt settlement companies

The Website

The National Debt Relief website is professional, well-organized, and highly promotional. It’s understandable that a debt settlement company would promote the advantages of debt settlement, but there is no clear disclosure of risks, and that’s not a positive sign.

We did spot two issues that raise questions.

In the FAQ section, we noted this quote:

“Depending on your personal situation and whether you have already missed payments to your creditors, debt settlement programs may have a negative impact on your credit score.”

This is not entirely honest. If your credit score is already badly damaged, debt settlement may not have a major impact. If your score is still reasonably good, debt settlement will almost certainly have a large and lasting negative impact.

In a section titled “How National Debt Relief Works with its Clients,” we note the following statement (bold type added for emphasis):

“Once you qualify for debt settlement, National Debt Relief will provide you with an agreement that spells out exactly what the company will do for you, what will be required from you and the cost of services. As soon as you sign the agreement, you’ll no longer be required to pay your creditors. Instead, National Debt Relief will deposit the money you send them into an escrow account that only you can control.”

This is simply not true, and it is potentially very deceptive. A debt is a legal obligation, and signing an agreement with a debt settlement company does not eliminate that obligation.

If your creditor agrees to a settlement, the obligation will end. From the time you stop making payments to the time a settlement is agreed upon, though, you will be violating a legal debt agreement.

That has consequences. Your missed payments will be reported to the credit bureaus, and accounts could be charged off and sent to collections. Your credit will suffer. A creditor could sue you, and if a court rules against you, your wages could be garnished.

These issues are additional indications that National Debt Relief may not be entirely straightforward about disclosing the risks of debt settlement.

Customer Service

You can reach National Debt Relief by toll-free phone at 800-300-9550 during these hours.

- Monday – Friday: 8:00 am – Midnight EST

- Sat: 10:00am – 10:00pm EST

- Sun: 10:00am – 9:00pm EST

You can also contact them through your customer dashboard on the website.

Customer reviews generally have very positive comments on the quality and efficiency of customer service.

Is National Debt Relief Trustworthy?

Any time you provide personal financial information to an outside company, there is some risk that the information could be compromised in a data breach. Some companies also actively sell information to marketing partners.

National Debt Relief states that they do not sell, rent, share, or trade personal information. They do not provide information on their data security systems, but there is no indication that data has been compromised in the past.

What are Customers Saying?

The Better Business Bureau (BBB) gives National Debt Relief an A+ rating, indicating a high level of responsiveness to customer complaints. The complaint page lists 253 complaints closed, with a response rate of 100%.

Trustpilot reviews show an average score of 4.7 of 5 stars from almost 36,000 reviews.

Positive reviews consistently praise the company’s work rate, customer service, and effectiveness. There are negative reviews from customers who did not have satisfactory experiences, but some appear to be from clients with unrealistic expectations or a poor understanding of the process.

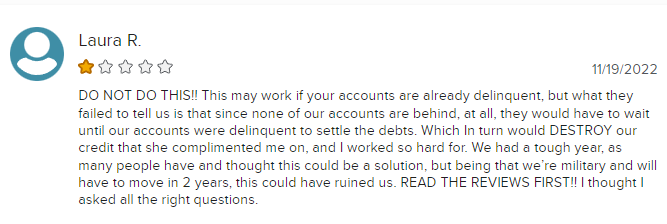

One red flag review stands out:

One of the primary responsibilities of any debt settlement company is to explain the risks inherent in the process, including the risk of credit damage. Recommending debt settlement to a client with good credit is usually not the best option for that particular client.

READ MORE: How debt settlement affects your credit score

Interested in National Debt Relief? Check out this video to learn the crucial questions you should ask.

The Bottom Line

If you have decided on debt settlement, National Debt Relief is a legitimate debt solution.

It’s not a perfect company — there are questions about risk disclosure practices, and there are claims on the website that are questionable at best — but they are a solid option if you’re truly devoted to becoming debt-free.

FAQs

If you choose debt settlement, you will stop making payments on your debts until you have saved enough to offer a settlement. Your missed payments will be reported to the credit bureaus. Accounts may be charged off and sent to collections. Your credit score will be damaged.

National Debt Relief works with unsecured debt, like credit card debt, medical debt, personal loans, payday loans, and private student loans. They cannot help with mortgages, car loans, other secured loans, or federal student loans.

National Debt Relief has extremely positive customer reviews and a generally good reputation in its industry. While the company shares the risks and disadvantages common to all debt settlement companies, it is one of the most credible companies in its industry. It even landed on Credit Summit’s list of best debt settlement companies. How does Accredited Debt Relief Compare to Other Debt Settlement Companies?